What Is Break Even Analysis and How to Calculate and Use It

A break-even analysis is a financial technique that aids a business in figuring out when it will become viable to provide a new service or product. Put another way, and it is a financial formula for figuring out how many goods or services a business should sell or provide to pay its expenses (particularly fixed costs).

Break-Even Analysis Definition

An organization is at break-even if all expenditures have been paid, but no money is being made or lost.

Break-even analysis is helpful when examining the relationship between variable costs, fixed costs, and income. A business with little fixed expenses often has a low sales break-even point. For instance, if two companies, XYZ Ltd. and ABC Ltd., are selling comparable items and XYZ Ltd. has fixed expenses of$10,000 while ABC Ltd. has fixed costs of $100,000, XYZ Ltd. will be able to break even with the sale of fewer products than ABC Ltd.

When to Use Break-Even Analysis

- Opening a new company: A break-even study is required before establishing a new company. It not only aids in determining if a new company concept is feasible but also forces the firm to be honest about expenses and serves as a foundation for pricing strategy.

- Making a new product: If a firm already has a business, it should still do a break-even analysis before introducing a new product, especially if it significantly increases costs.

- Business Model Change: A break-even study must be carried out when a firm is preparing to alter its business strategy, such as moving from wholesale to retail sales. A Break-Even analysis will assist in determining the selling price since expenses might fluctuate significantly.

Break-Even Analysis Benefits

- Recognize missing costs: You may overlook a few costs while planning a new company. To determine your break-even point, you may analyze all your financial obligations using a break-even analysis. This study limits unexpected events in the future or at least gets a corporation ready for them.

- Establish revenue goals: After completing the break-even analysis, you will learn how much you must sell to turn a profit. Thanks to this, you and your sales staff can establish more specific sales objectives.

- Make more informed choices: Entrepreneurs often base business judgments about their company on emotion. While emotion, or how you feel, is vital, it is insufficient. Being a successful entrepreneur requires making judgments that are supported by data.

- Fund your business: This research is essential to any business plan. If you wish to raise capital from outside investors, it's often crucial. To get money, you must show that your business concept is viable. Also, if the research is successful, you'll feel safe enough to take on the burden of various financing alternatives.

- Increased cost knowing the break-even point will help you set a higher product price. This technique is often used to provide goods at the most profitable prices possible without increasing existing costs.

- Paying fixed costs can cover all fixed expenses using a break-even analysis.

Limitations of Break-Even Analysis

The most crucial point to remember is that market demand is not considered by break-even analysis. Knowing that 500 units must be sold to break even does not indicate if or when you can sell those 500 units. Refrain from allowing your enthusiasm for the company's concept or a novel product to compel you to overlook this fundamental reality.

On the other hand, you must choose how much time and effort you are prepared to put out to achieve the break-even point. For instance, are you ready to devote a significant portion of your sales team's time and energy over months to complete the break-even point? Or would it be more efficient and economical to produce and sell something else?

| Get Started Now to Grow Your Online Business with the Best AliExpress Dropshipping Tool - DSers! |

Consider altering your pricing plan to sell products more quickly if you discover that demand for the product is weak. Discounted prices, however, may push you over where you break even. If you don't take care, you'll move goods more quickly at a cheaper cost, but will have to pay higher variable expenses to create more units to break even.

Critical Components of a Break-Even Analysis

The following are the Key Components of a Break-Even Analysis:

Fixed Cost

Fixed Costs are also known as Overhead costs. These overhead costs are incurred after the choice to begin an economic activity is made, and they are directly tied to the quality but not the amount of output.

Interest, taxes, wages, rent, depreciation expenses, labor costs, energy costs, and other fixed expenditures are just a few examples. These expenses are set regardless of productivity. Costs must be paid even if there is no output.

Variable Cost

Costs that will change according to the production volume are known as variable costs. These expenses include the price of raw materials, the cost of packing, the cost of gasoline, and any other expenses directly associated with manufacturing.

Contribution of Break-Even Analysis

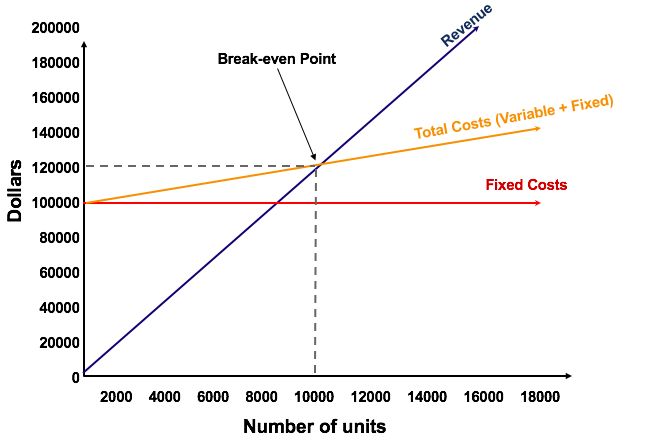

Divided by the contribution per unit, the total fixed production costs provide the fundamental equation for break-even analysis (price per unit less the variable costs).

- Contribution per unit = Selling Price per unit – Variable Cost Per Unit

Break-Even Point

- Break-Even Point in Quantity BEP=FC Contribution Per Unit OR FCP-VC

- *FC (Total Fixed Cost) ; VC (Variable Cost Per Unit) ; P (Average Price per unit)

Contribution Margin

The contribution margin of a product is another topic covered by break-even analysis. The contribution margin differs between the selling price and all variable expenses. For example, the contribution margin of a product with a price of $100, total variable expenses of $60 per product, and fixed costs of $25 per product, is $40. ($100 –$60). This rupee of forty represents the income gathered to pay the fixed expenses. Fixed expenses are excluded from the computation of the contribution margin.

Why Is Break-Even Analysis Useful

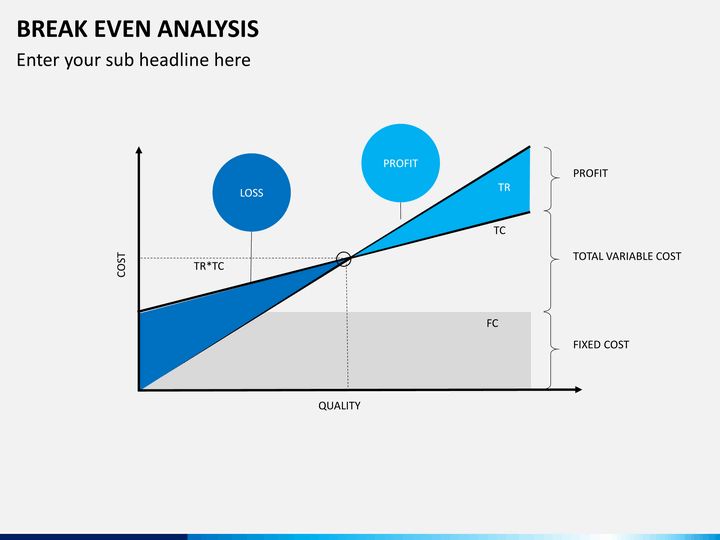

- After achieving breakeven, it helps assess the company's residual or underused capacity. This will demonstrate the most significant profit that may be made on a specific item or service.

- Determining the effects of switching from manual to automated processes on profit (a fixed cost replaces a variable cost).

- If a product's price changes, it may be used to calculate the difference in earnings.

- Finding out how much damage may be incurred during a sales slump is helpful.

Break-even analysis is also beneficial for understanding a company's total capacity to turn a profit. When a corporation's breakeven point is close to its maximum sales level, it means that, even in the best-case scenario, it is almost impossible for the company to profit.

Thus, the management must regularly check the breakeven point. Where feasible, this monitoring lowers the breakeven point.

How to Monitor Break-Even Point

- Price analysis: Reduce or completely stop using coupons and other price reduction offers, since they raise the breakeven point.

- Technological analysis: Applying any technology that may improve corporate productivity and expand capacity without incurring additional costs.

- Cost analysis: It might be beneficial to continually assess all fixed expenses to see if any can be cut. Review the overall variable expenses to determine if any may be cut. The margin will rise, and the breakeven point will fall due to this study.

- Margin analysis: Encourage sales of the goods with the most significant margins (most considerable contribution to earnings) and pay strict attention to product margins to lower the breakeven point.

- Outsourcing: Try to outsource such an operation (where feasible) if it has a fixed cost, since doing so lowers the breakeven point.

How to Lower your Break-Even Point

Increasing pricing and reducing expenses are the two main strategies for lowering your break-even point. Neither should be carried out in collaboration. Consider your alternatives carefully regarding pricing strategies and consumer psychology to avoid increasing product sales at the expense of revenue.

To avoid harm to your brand, consider all expenses, such as the related quality and delivery, before reducing them. Outsourcing goods or services may help keep prices down as demand or volume rises.

Conclusion

Making wise business choices requires doing a break-even analysis. So do a break-even study the next time you're considering establishing a new company or adjusting to your current one to be better prepared.

Company

Company

Why Choose DSers

Why Choose DSers

Blog

Blog

Help Center

Help Center

Live Chat

Live Chat